Chinese shadow bank exposed to troubled property developers

Receive free Chinese business & finance updates

We’ll send you a myFT Daily Digest email rounding up the latest Chinese business & finance news every morning.

The Chinese shadow bank at the heart of concerns over missed payments to customers has lent money to several of the country’s struggling property developers, according to a Financial Times analysis of legal and company filings.

The connections between Zhongrong, a giant of China’s $3tn shadow finance industry, and property developers have fuelled fears of spillover effects from a slowdown in the real estate sector, which accounts for more than a quarter of China’s economic activity.

This has added to mounting concerns about the state of China’s economy, which is struggling to recover after the Covid-19 pandemic.

Zhongrong and other shadow banks in the so-called trust industry sell high-yield savings products to retail investors and companies. They then lend the savings to companies across China, including property developers.

An estimated 11 per cent of Zhongrong’s assets are invested in the property sector, the company has said, but it does not provide information on any of its specific investments, and data across the wider industry is frequently lacking in transparency.

Zhongrong did not disclose its missed payments, and they were instead made public through stock exchange filings by listed companies.

Legal filings from 2022 and 2023 examined by the FT show Zhongrong has pursued more than Rmb8.7bn ($1.2bn) in claims against Sunac, formerly one of China’s largest developers, which defaulted in 2022. Sunac reached an offshore debt restructuring plan in March. It is unclear what, if any, settlement Zhongrong reached with Sunac.

Zhongrong delayed payments on two products due in March 2021 and April 2022, according to a disclosure in April from textile chemicals company Zhejiang Jihua. State media reports linked the products to real estate projects developed by China Fortune Land Development and Sunac, respectively.

In December 2020 Zhongrong lent money in the form of a Rmb1.5bn perpetual bond to China Fortune Land Development, according to the latter’s company filing. The company, one of China’s top developers, defaulted on its international debts two months later.

Zhongrong has also lent an unknown sum to Yango, another major developer that defaulted in 2022. It was repaid Rmb3.3bn when the project related to the loan was sold, according to a Yango filing in June last year.

In May 2022 Zhongrong sued Evergrande and other developers over a loan contract dispute of Rmb1.9bn, according to a 2022 report of Evergrande’s bonds. It is unclear what further exposure Zhongrong has to Evergrande, the world’s most indebted developer. Last month the property group said it faced more than 2,000 lawsuits worth Rmb30mn or more, with a total value of about Rmb535bn.

Zhongrong has had trouble securing repayments from at least one local government, whose high debts are a major concern for Beijing. A government investment fund in the city of Xi’an said in a July filing that it had delayed repayment of a Rmb900m loan to Zhongrong, blaming issues with “land development”.

Zhongrong has total assets of Rmb629bn, according to its 2022 annual report. It is the only large trust company with more than 10 per cent of its overall exposure in real estate.

In a statement on Friday, Zhongrong acknowledged it had been unable to pay some of its products on time and said it had entered into an agreement with state-backed Citic Trust and China Construction Bank Trust, under which they would provide Zhongrong with “entrusted management services”.

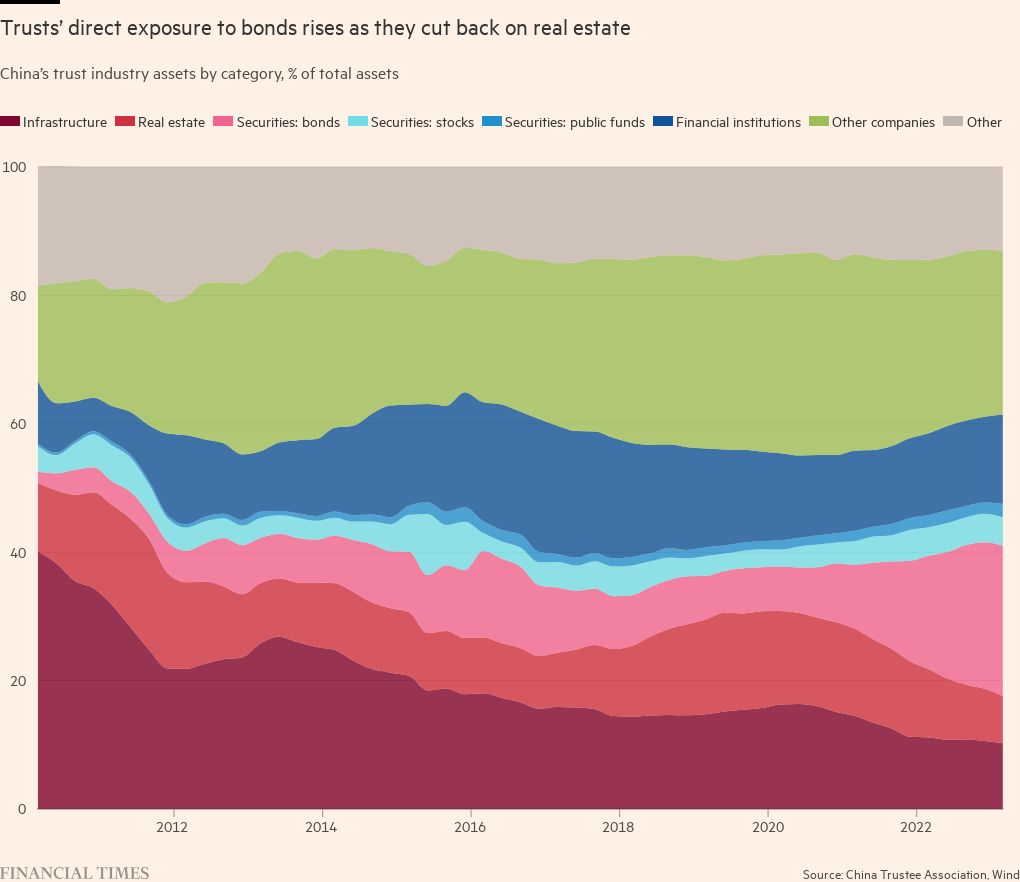

The overall trust industry in China, which includes 68 companies, has total assets of Rmb21tn and direct exposure to real estate of Rmb1.1tn as of the first quarter of this year, according to the China Trustee Association.

This data counts bonds, which are often issued by property developers, in a separate category and does not include figures for local government financing vehicles. Trust companies’ exposure to bonds has more than trebled since mid-2020, the data shows.

“There’s no breakdown of how many of the bonds’ [proceeds] are invested in the property sector,” said one analyst covering the sector, who asked not to be named. “The real exposure could be higher than what you’re seeing for property itself.”

Zhongrong, Sunac, Evergrande, China Fortune Land Development, Yango, the Xi’an local government fund and Zhejiang Jihua did not respond to requests for comment.

Additional reporting by Andy Lin in Hong Kong

Summarize this content to 100 words Receive free Chinese business & finance updatesWe’ll send you a myFT Daily Digest email rounding up the latest Chinese business & finance news every morning.The Chinese shadow bank at the heart of concerns over missed payments to customers has lent money to several of the country’s struggling property developers, according to a Financial Times analysis of legal and company filings.The connections between Zhongrong, a giant of China’s $3tn shadow finance industry, and property developers have fuelled fears of spillover effects from a slowdown in the real estate sector, which accounts for more than a quarter of China’s economic activity.This has added to mounting concerns about the state of China’s economy, which is struggling to recover after the Covid-19 pandemic.Zhongrong and other shadow banks in the so-called trust industry sell high-yield savings products to retail investors and companies. They then lend the savings to companies across China, including property developers.An estimated 11 per cent of Zhongrong’s assets are invested in the property sector, the company has said, but it does not provide information on any of its specific investments, and data across the wider industry is frequently lacking in transparency.Zhongrong did not disclose its missed payments, and they were instead made public through stock exchange filings by listed companies.Legal filings from 2022 and 2023 examined by the FT show Zhongrong has pursued more than Rmb8.7bn ($1.2bn) in claims against Sunac, formerly one of China’s largest developers, which defaulted in 2022. Sunac reached an offshore debt restructuring plan in March. It is unclear what, if any, settlement Zhongrong reached with Sunac.You are seeing a snapshot of an interactive graphic. This is most likely due to being offline or JavaScript being disabled in your browser.Zhongrong delayed payments on two products due in March 2021 and April 2022, according to a disclosure in April from textile chemicals company Zhejiang Jihua. State media reports linked the products to real estate projects developed by China Fortune Land Development and Sunac, respectively.In December 2020 Zhongrong lent money in the form of a Rmb1.5bn perpetual bond to China Fortune Land Development, according to the latter’s company filing. The company, one of China’s top developers, defaulted on its international debts two months later.Zhongrong has also lent an unknown sum to Yango, another major developer that defaulted in 2022. It was repaid Rmb3.3bn when the project related to the loan was sold, according to a Yango filing in June last year. In May 2022 Zhongrong sued Evergrande and other developers over a loan contract dispute of Rmb1.9bn, according to a 2022 report of Evergrande’s bonds. It is unclear what further exposure Zhongrong has to Evergrande, the world’s most indebted developer. Last month the property group said it faced more than 2,000 lawsuits worth Rmb30mn or more, with a total value of about Rmb535bn.You are seeing a snapshot of an interactive graphic. This is most likely due to being offline or JavaScript being disabled in your browser.Zhongrong has had trouble securing repayments from at least one local government, whose high debts are a major concern for Beijing. A government investment fund in the city of Xi’an said in a July filing that it had delayed repayment of a Rmb900m loan to Zhongrong, blaming issues with “land development”.Zhongrong has total assets of Rmb629bn, according to its 2022 annual report. It is the only large trust company with more than 10 per cent of its overall exposure in real estate.In a statement on Friday, Zhongrong acknowledged it had been unable to pay some of its products on time and said it had entered into an agreement with state-backed Citic Trust and China Construction Bank Trust, under which they would provide Zhongrong with “entrusted management services”.The overall trust industry in China, which includes 68 companies, has total assets of Rmb21tn and direct exposure to real estate of Rmb1.1tn as of the first quarter of this year, according to the China Trustee Association.RecommendedThis data counts bonds, which are often issued by property developers, in a separate category and does not include figures for local government financing vehicles. Trust companies’ exposure to bonds has more than trebled since mid-2020, the data shows.“There’s no breakdown of how many of the bonds’ [proceeds] are invested in the property sector,” said one analyst covering the sector, who asked not to be named. “The real exposure could be higher than what you’re seeing for property itself.” Zhongrong, Sunac, Evergrande, China Fortune Land Development, Yango, the Xi’an local government fund and Zhejiang Jihua did not respond to requests for comment.Additional reporting by Andy Lin in Hong Kong

https://www.ft.com/content/5948fd27-8195-4974-879e-125546112be3 Chinese shadow bank exposed to troubled property developers